Nothing in life is certain except death and taxes. — Benjamin Franklin

That saying still rings true roughly 300 years after the former statesman coined it. Yet, by formulating a tax-efficient investment and distribution strategy, retirees may keep more of their hard-earned assets for themselves and their heirs. Here are a few suggestions for effective money management during your later years.

Less Taxing Investments

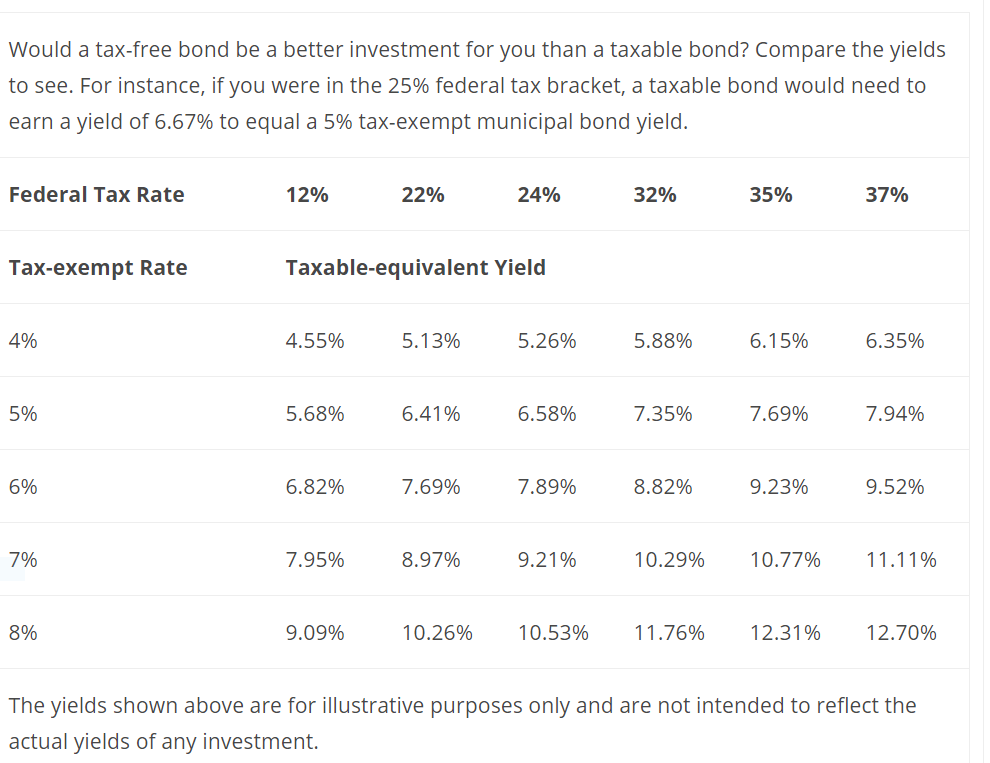

Municipal bonds, or “munis,” have long been appreciated by retirees seeking a haven from taxes and stock market volatility. In general, the interest paid on municipal bonds is exempt from federal taxes and sometimes state and local taxes as well (see table).1 The higher your tax bracket, the more you may benefit from investing in munis.

Also, consider investing in tax-managed mutual funds. Managers of these funds pursue tax efficiency by employing a number of strategies. For instance, they might limit the number of times they trade investments within a fund or sell securities at a loss to offset portfolio gains. Equity index funds may also be more tax efficient than actively managed stock funds due to a potentially lower investment turnover rate.

It’s also important to review which types of securities are held in taxable versus tax-deferred accounts. Why? Because the maximum federal tax rate on some dividend-producing investments and long-term capital gains is 20%.3 In light of this, many financial experts recommend keeping real estate investment trusts (REITs), high-yield bonds, and high-turnover stock mutual funds in tax-deferred accounts. Low-turnover stock funds, municipal bonds, and growth or value stocks may be more appropriate for taxable accounts.

The Tax-exempt Advantage: When Less May Yield More

Which Securities to Tap First?

Another major decision facing retirees is when to liquidate various types of assets. The advantage of holding on to tax-deferred investments is that they compound on a before-tax basis and therefore have greater earning potential than their taxable counterparts.

On the other hand, you’ll need to consider that qualified withdrawals from tax-deferred investments are taxed at ordinary federal income tax rates of up to 37%, while distributions — in the form of capital gains or dividends — from investments in taxable accounts are taxed at a maximum 20%.* (Capital gains on investments held for less than a year are taxed at regular income tax rates.)

For this reason, it’s beneficial to hold securities in taxable accounts long enough to qualify for the favorable long-term rate. And, when choosing between tapping capital gains versus dividends, long-term capital gains are more attractive from an estate planning perspective because you get a step-up in basis on appreciated assets at death.

It also makes sense to take a long view with regard to tapping tax-deferred accounts. Keep in mind, however, the deadline for taking annual required minimum distributions (RMDs).

The Ins and Outs of RMDs

The IRS mandates that you begin taking an annual RMD from traditional individual retirement accounts (IRAs) and employer-sponsored retirement plans after you reach age 70½. The premise behind the RMD rule is simple — the longer you are expected to live, the less the IRS requires you to withdraw (and pay taxes on) each year.

RMDs are now based on a uniform table, which takes into consideration the participant’s and beneficiary’s lifetimes, based on the participant’s age. Failure to take the RMD can result in a tax penalty equal to 50% of the required amount. Tip: If you’ll be pushed into a higher tax bracket at age 70½ due to the RMD rule, it may pay to begin taking withdrawals during your sixties.

Unlike traditional IRAs, Roth IRAs do not require you to begin taking distributions by age 70½.2 In fact, you’re never required to take distributions from your Roth IRA, and qualified withdrawals are tax free.2 For this reason, you may wish to liquidate investments in a Roth IRA after you’ve exhausted other sources of income. Be aware, however, that your beneficiaries will be required to take RMDs after your death.

Estate Planning and Gifting

There are various ways to make the tax payments on your assets easier for heirs to handle. Careful selection of beneficiaries of your accounts is one example. If you do not name a beneficiary, your assets could end up in probate, and your beneficiaries could be taking distributions faster than they expected. In most cases, spousal beneficiaries are ideal because they have several options that aren’t available to other beneficiaries, including the marital deduction for the federal estate tax.

Also, consider transferring assets into an irrevocable trust if you’re close to the threshold for owing estate taxes. In 2019, the federal estate tax applies to all estate assets over $11.4 million. Assets in an irrevocable trust are passed on free of estate taxes, saving heirs thousands of dollars. Tip: If you plan on moving assets from tax-deferred accounts, do so before you reach age 70½, when RMDs must begin.

Finally, if you have a taxable estate, you can give up to $15,000 per individual ($30,000 per married couple) each year to anyone tax free. Also, consider making gifts to children over age 14, as dividends may be taxed — or gains tapped — at much lower tax rates than those that apply to adults. Tip: Some people choose to transfer appreciated securities to custodial accounts (UTMAs and UGMAs) to help save for a grandchild’s higher education expenses.

Strategies for making the most of your money and reducing taxes are complex. Your best recourse? Plan ahead and consider meeting with a competent tax advisor, an estate attorney, and a financial professional to help you sort through your options.

Source/Disclaimer:

1Capital gains from municipal bonds are taxable, and interest income may be subject to the alternative minimum tax.

2Withdrawals prior to age 59½ are generally subject to a 10% additional tax.

3Income from investment assets may be subject to an additional 3.8% Medicare tax, applicable to single-filer taxpayers with modified adjusted gross income of over $200,000 and $250,000 for joint filers.

Required Attribution

Because of the possibility of human or mechanical error by DST Systems, Inc. or its sources, neither DST Systems, Inc. nor its sources guarantees the accuracy, adequacy, completeness or availability of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. In no event shall DST Systems, Inc. be liable for any indirect, special or consequential damages in connection with subscriber’s or others’ use of the content.

© 2019 DST Systems, Inc. Reproduction in whole or in part prohibited, except by permission. All rights reserved. Not responsible for any errors or omissions.